research

Generació de la corba d'oferta a partir de les dades públiques del MIBEL

Wed, 02/11/2009 - 12:40 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Glòria Casanellas; Cristina Corchero: F.-Javier Heredia |

| Pages | 27 |

| Date | 11/2008 |

| Reference | Research Report 2008/16, Dept. of Statistics and Operations Research, Universitat Politècnica de Catalunya |

| City | Barcelona |

| Key Words | research; electricity markets; MIBEL; bidding |

| Export | Tagged XML BibTex |

Generació de figures eps a partir dels resultats d'AMPL

Wed, 02/11/2009 - 12:38 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Marcos-J. Rider; Glòria Casanellas; F.-Javier Heredia |

| Pages | 8 |

| Date | 11/2008 |

| Reference | Research Report DR 2008/15, Dept. of Statistics and Operations Research, Universitat Politècnica de Catalunya |

| City | Barcelona |

| Key Words | research; LaTeX |

| Export | Tagged XML BibTex |

Beca FPI-MICINN de doctorado en Mercados Eléctricos

Mon, 01/12/2009 - 12:15 — admin

(ATENCIÓN: CONVOCATORIA CERRADA Y RESUELTA) . ACCESO A LA CONVOCATORIA .

El Grupo de Optimitzación Numérica y Modelización (GNOM) del Departament d'Estadística I Investigació Operativa de la Universidad Poltécnica de Catalunya, dispone de una Beca de Formación de Personal Investigador (FPI) del Ministerio de Ciencia e Innovación, para la realización de una tesis doctoral dentro de un proyecto de investigación sobre Optimización de Mercados Eléctricos financiado por el Plan Nacional de I+D+i. La duración de la beca es de hasta cuatro años.

Optimal Bidding Strategies for Thermal and Generic Programming Units in the Day-ahead Electricity Market

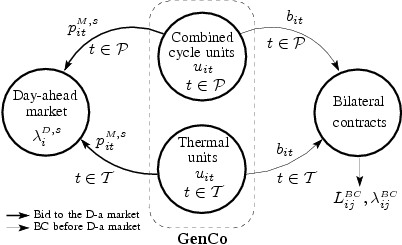

Fri, 12/19/2008 - 11:26 — admin In this new work submitted to the journal IEEE Transactions on Power Systems, the authors, prof. F.-Javier Heredia, Dr. Marcos.-J Rider and Ms. Cristina Corchero developed, within the general stochastic programming framework, a new optimal bid model for both thermal and generic programmingn units (also known as Virtual Powewr Plants) taken into account the most recent regulation rules of the Spanish peninsular system MIBEL. This model allows a price-taker generation company to decide the unit commitment and sale bids of the thermal units, the optimal sale/purchase bids of the Virtual Power Plant and the economic dispatch of the bilateral contracts between all the programming units (thermal and generic). Download the full text at http://hdl.handle.net/2117/2282

In this new work submitted to the journal IEEE Transactions on Power Systems, the authors, prof. F.-Javier Heredia, Dr. Marcos.-J Rider and Ms. Cristina Corchero developed, within the general stochastic programming framework, a new optimal bid model for both thermal and generic programmingn units (also known as Virtual Powewr Plants) taken into account the most recent regulation rules of the Spanish peninsular system MIBEL. This model allows a price-taker generation company to decide the unit commitment and sale bids of the thermal units, the optimal sale/purchase bids of the Virtual Power Plant and the economic dispatch of the bilateral contracts between all the programming units (thermal and generic). Download the full text at http://hdl.handle.net/2117/2282

Optimal Bidding Strategies for Thermal and Generic Programming Units in the Day-ahead Electricity Market

Fri, 12/19/2008 - 10:57 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Heredia, F.-Javier, Rider, Marcos.-J., Corchero, C. |

| Pages | 12 |

| Date | 11/2008 |

| Reference | Research report DR 2008/13, Dept. of Statistics and Operations Research. E-Prints UPC, http://hdl.handle.net/2117/2468. Universitat Politècnica de Catalunya |

| Prepared for | Published on august 2010 at IEEE Transactions on Power Systems |

| Key Words | research; stochastic programming; electricity markets; day-ahead market, bilateral contracts; Virtual Power Plants; optimal bid |

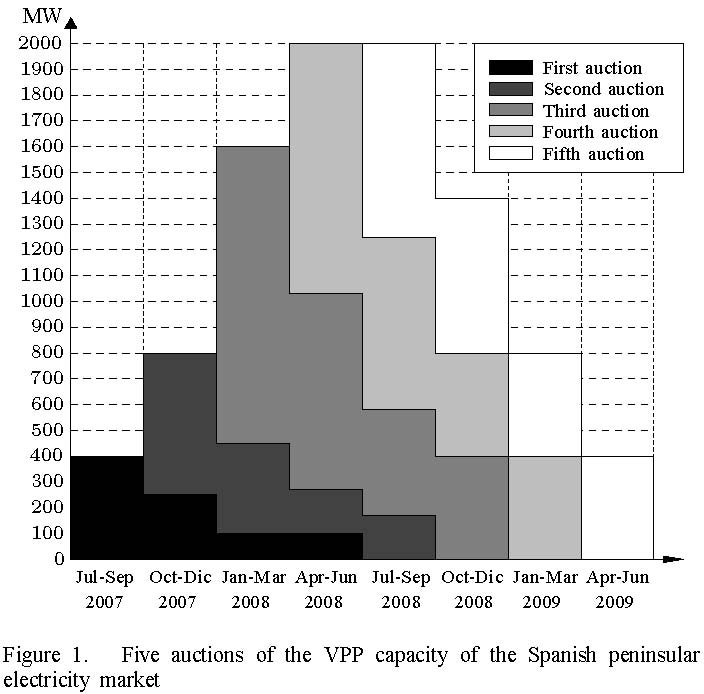

| Abstract | This paper develops a stochastic programming model that integrates the day-ahead optimal bidding problem with the most recent regulation rules of the Iberian Electricity Market (MIBEL) for bilateral contracts, with a special consideration for the new mechanism to balance the competition of the production market, namely virtual power plants auctions (VPP). The model allows a price-taker generation company to decide the unit commitment of the thermal units, the economic dispatch of the bilateral contracts between the thermal units and the generic programming unit (GPU) and the optimal sale/purchase bids for all units (thermal and generic) observing the MIBEL regulation. The uncertainty of the spot prices is represented through scenario sets built from the most recent real data using scenario reduction techniques. The model was solved with real data from a Spanish generation company and spot prices, and the results are reported and analyzed. |

| URL | Click Here |

| Export | Tagged XML BibTex |

A decision support for a Price-Taker producer operating on Day-Ahead and Physical Derivatives Electricity Markets

Wed, 12/17/2008 - 12:18 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Vespucci, M.T.; Corchero, C.; Innorta, M.; Heredia, F.-Javier |

| Pages | 10 |

| Date | 12/2008 |

| Reference | Working paper n12/MS-2008, Dipartimento di Ingegneria dell'Informazione e Metodi Matematici, Università degli Studi di Bergamo |

| City | Bergamo, Italy |

| Key Words | research; stochastic programming; electricity markets; futures contracts; hydro-thermal |

| URL | Click Here |

| Export | Tagged XML BibTex |

New research project granted by the "Ministerio de Ciencia e Innovación"

Fri, 11/07/2008 - 20:28 — admin  The GNOM research group of the UPC has been granted by the Ministerio de Ciencia e Innovación of the Spanish Government to develop the research project Short - and Medium Term Multimarket Optimal Electricity Generation Planning With Risk and Environmental Constraints. This is a three years project starting on january 2009 with an assigned budget of 130.000€, that extens the work done in several previous research projects . The leader of the project is Prof. F. Javier Heredia, and participate several researchers from the Universidad Politècnica de Catalunya, Universidad del País Vasco, Universidade Estadual de Campinas-UNICAMP, University of Edinburgh and Norwegian University of Science and Technology.The spanish electrical utilities Unión Fenosa and Gas Natural are also involved in the project as external observers and promoters. Follow this link to know more about this project.

The GNOM research group of the UPC has been granted by the Ministerio de Ciencia e Innovación of the Spanish Government to develop the research project Short - and Medium Term Multimarket Optimal Electricity Generation Planning With Risk and Environmental Constraints. This is a three years project starting on january 2009 with an assigned budget of 130.000€, that extens the work done in several previous research projects . The leader of the project is Prof. F. Javier Heredia, and participate several researchers from the Universidad Politècnica de Catalunya, Universidad del País Vasco, Universidade Estadual de Campinas-UNICAMP, University of Edinburgh and Norwegian University of Science and Technology.The spanish electrical utilities Unión Fenosa and Gas Natural are also involved in the project as external observers and promoters. Follow this link to know more about this project.

Short- and Medium-Term Multimarket Optimal Electricity Generation Planning with Risk and Environmental Constraints (DPI2008-02153)

Fri, 11/07/2008 - 19:57 — admin| Publication Type | Funded research projects |

| Year of Publication | 2008 |

| Authors | F.-Javier Heredia |

| Type of participation | Project leader |

| Duration | 01/2009-12/2011 |

| Call | Proyectos de Investigación Fundamental no Orientada 2008. IV Plan Nacional de I+D+i (2008-2011) |

| Funding organization | Ministerio de Ciencia e Innovación, Gobierno de España |

| Partners | Unión Fenosa, Gas Natural, Universidad Politècnica de Catalunya, Universidad del País Vasco, Universidade Estadual de Campinas-UNICAMP, University of Edinburgh, Norwegian University of Science and Technology. |

| Full time researchers | 6 EDP |

| Budget | 157.300'00€ |

| Project code | DPI2008-02153 |

| Key Words | research; stochastic programming; electricity markets; risc; multimarket; environmental constraints; project; public; competitive; micinn; energy |

| URL | Click Here |

| Export | Tagged XML BibTex |

A stochastic programming model for the optimal electricity market bid problem with bilateral contracts for thermal and CC units

Thu, 10/09/2008 - 17:48 — admin

This work, co-authored by Dr. Marcos.-J Rider and Ms. Cristina Corchero and submitted to the journal Annals of Operations Research, developed a stochastic programming model that integrated the most recent regulation rules of the Spanish peninsular system for bilateral contracts in the day-ahead optimal bid problem. This model allows a price-taker generation company to decide the unit commitment of the thermal and combined cycle programming units, the economic dispatch of the bilateral contracts between all the programming units and the optimal sale bid by observing the Spanish peninsular regulation. See the full text at http://hdl.handle.net/2117/2282

A stochastic programming model for the optimal electricity market bid problem with bilateral contracts for thermal and combined cycle units

Thu, 10/09/2008 - 17:27 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Heredia, F.-Javier, Rider, Marcos.-J., Corchero, C. |

| Pages | 18 |

| Date | 10/2008 |

| Reference | Group on Numerical Optimization and Modelling, E-Prints UPC, http://hdl.handle.net/2117/2282. UPC. |

| Prepared for | Accepted for publication in Annals of Operations Research (2011) |

| City | Barcelona |

| Key Words | combined cycle units; optimal bid; bilateral contracts; day-ahead market; electricity markets; stochastic programming; modeling language; research |

| Abstract | This paper developed a stochastic programming model that integrated the most recent regulation rules of the Spanish peninsular system for bilateral contracts in the day-ahead optimal bid problem. Our model allows a price-taker generation company to decide the unit commitment of the thermal and combined cycle programming units, the economic dispatch of the BC between all the programming units and the optimal sale bid by observing the Spanish peninsular regulation. The model was solved using real data of a typical generation company and a set of scenarios for the Spanish market price. The results are reported and analyzed. |

| URL | Click Here |

| Export | Tagged XML BibTex |