bilateral contracts

A stochastic programming model for the optimal electricity market bid problem with bilateral contracts for thermal and CC units

Thu, 10/09/2008 - 17:48 — admin

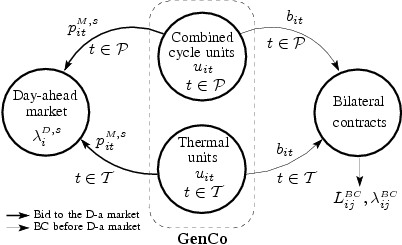

This work, co-authored by Dr. Marcos.-J Rider and Ms. Cristina Corchero and submitted to the journal Annals of Operations Research, developed a stochastic programming model that integrated the most recent regulation rules of the Spanish peninsular system for bilateral contracts in the day-ahead optimal bid problem. This model allows a price-taker generation company to decide the unit commitment of the thermal and combined cycle programming units, the economic dispatch of the bilateral contracts between all the programming units and the optimal sale bid by observing the Spanish peninsular regulation. See the full text at http://hdl.handle.net/2117/2282

A stochastic programming model for the optimal electricity market bid problem with bilateral contracts for thermal and combined cycle units

Thu, 10/09/2008 - 17:27 — admin| Publication Type | Report |

| Year of Publication | 2008 |

| Authors | Heredia, F.-Javier, Rider, Marcos.-J., Corchero, C. |

| Pages | 18 |

| Date | 10/2008 |

| Reference | Group on Numerical Optimization and Modelling, E-Prints UPC, http://hdl.handle.net/2117/2282. UPC. |

| Prepared for | Accepted for publication in Annals of Operations Research (2011) |

| City | Barcelona |

| Key Words | combined cycle units; optimal bid; bilateral contracts; day-ahead market; electricity markets; stochastic programming; modeling language; research |

| Abstract | This paper developed a stochastic programming model that integrated the most recent regulation rules of the Spanish peninsular system for bilateral contracts in the day-ahead optimal bid problem. Our model allows a price-taker generation company to decide the unit commitment of the thermal and combined cycle programming units, the economic dispatch of the BC between all the programming units and the optimal sale bid by observing the Spanish peninsular regulation. The model was solved using real data of a typical generation company and a set of scenarios for the Spanish market price. The results are reported and analyzed. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Optimal thermal and virtual power plants operation in the day-ahead electricity market.

Tue, 06/10/2008 - 12:22 — admin| Publication Type | Conference Paper |

| Year of Publication | 2008 |

| Authors | F.-Javier Heredia; Marcos-J. Rider; Cristina Corchero |

| Conference Name | APMOD 2008 International Conference on Applied Mathematical Programming and Modelling |

| Series Title | APMOD2008 CONFERENCE BOOK |

| Pagination | 21 |

| Conference Date | 27-30/05/2008 |

| Conference Location | Comenius University, Bratislava, Slovak Republic |

| Type of Work | Contributed presentation |

| Key Words | stochastic programming; electricity markets; day-ahead market; bilateral contracts; Virtual Power Plant; Generic Programming Unit; MIBEL; modellization; research |

| Abstract | The new rules of the electrical energy production market operation of the Iberic Electricity Market MIBEL (mainland Spanish and Portuguese systems), for the diary and intra-diary market (July 2007), bring new challenges in the modeling and solution of the production market operation. Aiming to increase the proportion of electricity that is purchased through bilateral contracts with duration of several months and intending to stimulate liquidity in forward electricity markets, the Royal Decree 1634/2006, dated December 29th, 2006 imposes to Endesa and Iberdrola (the two dominant utility companies in the Spanish peninsular Markets) to hold a series of five auctions offering virtual power plant (VPP) capacity to any party who is a member of the MIBEL. Other experience of the application of VPP auctions can be seen in France, Belgium and Germany. In Spain, the VPP capacity means that the buyer of this product will have the capacity to generate MWh at his disposal. The buyer can exercise the right to produce against an exercise price that is set in advance, by paying an option premium. So although Endesa and Iberdrola still own the power plants, part of their capacity to produce will be at the disposal of the buyers of VPP. VPP capacity is represented by a set of hourly call options giving the buyer the right to nominate energy for delivery at a pre-defined exercise price. There will be baseload and peakload contracts with different exercise prices. The energy resulting from the exercise of the VPP options can be used by buyers in several ways: (a) national and international bilateral contracts prior to the day-ahead market; (b) bids to the day-ahead market and (c) national bilateral contracts after the day-ahead market. In order to operate the VPP options each buyer agent will have a Generic Unit (GU). This work develops an stochastic programming model for a Generation Company (GenCo) to find the optimal management of a VPP in the day-ahead electricity market under the most recent bilateral contracts regulation rules of MIBEL energy market. |

| Export | Tagged XML BibTex |

Stochastic programming model for the day-ahead bid and bilateral contracts settlement problem

Tue, 06/10/2008 - 11:57 — admin| Publication Type | Conference Paper |

| Year of Publication | 2008 |

| Authors | F.-Javier Heredia; Marcos-J. Rider; Cristina Corchero |

| Conference Name | International Workshop on Operational Research 2008 |

| Series Title | I.W.OR. International Workshop on Operations Research |

| Pagination | 79 |

| Conference Date | 5-7/06/2008 |

| Publisher | Dept. of Statistics and Operational Research, Univ. Rey Juan Carlos. |

| Conference Location | Dept. of Statistics and Operational Research, Univ. Rey Juan Carlos, Madrid, Spain |

| Type of Work | Invited presentation |

| ISBN Number | 978-84-691-3994-3 |

| Key Words | stochastic programming; electricity markets; day-ahead market; bilateral contracts; Virtual Power Plant; Generic Programming Unit; MIBEL; modellization; research |

| Abstract | The new rules of electrical energy production market operation of the Spanish peninsular system (MIBEL) from the July 2007, bring new challenges in the modeling and solution of the production market operation. In order to increase the proportion of electricity that is purchased through bilateral contracts and to stimulate liquidity in forward electricity markets, the MIBEL rules imposes to the dominant utility companies in the Spanish peninsular Markets to hold a series of auctions offering virtual power plant (VPP) capacity to any party who is a member of the Spanish peninsular electricity market. In Spain, the VPP capacity means that the buyer of this product will have the capacity to generate MWh at his disposal. The energy resulting from the exercise of the VPP options can be used by buyers in several ways: covering national and international bilateral contracts prior to the day-ahead market; bidding to the day-ahead market and covering national bilateral contracts after the day-ahead market. This work develops a stochastic programming model that integrates the most recent regulation rules of the Spanish peninsular system for bilateral contracts, especially VPP auctions, in the day-ahead optimal bid problem. The model currently developed allows a price-taker generation company to decide the unit commitment of the thermal units, the economic dispatch of the bilateral contracts between the thermal and generic units and the optimal bid observing the Spanish peninsular regulation. The scenario tree representing the uncertainty of the spot prices is built applying reduction techniques to the tree obtained from an ARIMA model. The model was solved with real data of a Spanish generation company and market prices. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Planificación de la generación eléctrica a corto y largo plazo en un mercado liberalizado con contratos bilaterales (DPI2005-09117-C02-01).

Wed, 10/24/2007 - 23:39 — admin| Publication Type | Funded research projects |

| Year of Publication | 2005 |

| Authors | F.-Javier Heredia |

| Type of participation | Full time researcher |

| Duration | 01/2006-12/2008 |

| Funding organization | Ministerio de Educación y Ciencia |

| Partners | Departament d'Estadística i Investigació Operativa, Universidad Politèctica de Catalunya; Unión Fenosa |

| Full time researchers | 5 |

| Budget | 289.408'00€ |

| Project code | DPI2005-09117-C02-01 |

| Key Words | research; stochastic programming; electricity markets; future contracts; bilateral contracts; regulation markets; project; public; competitive; micinn; energy |

| Abstract | The project aims at two new features: the simultaneous consideration of bidding power to the liberalized market and of bilateral contracts (between a generation company and a consumer client), given the future elimination of the current regulations discouraging bilateral contracts, and the developement of optimization procedures more efficient than those employed now to solve these problems. This higher efficiency will allow a more accurate modeling and solving larger real problems in reasonable CPU time. In this project, both modeling languages and commercially available solvers in the one hand, and our own optimization algorithms in the other are employed. The algorithms to be developed include the use of: interior-point methods, global optimization, column-generation methods, and Lagrangian relaxation procedures employing dual methods |

| URL | Click Here |

| Export | Tagged XML BibTex |